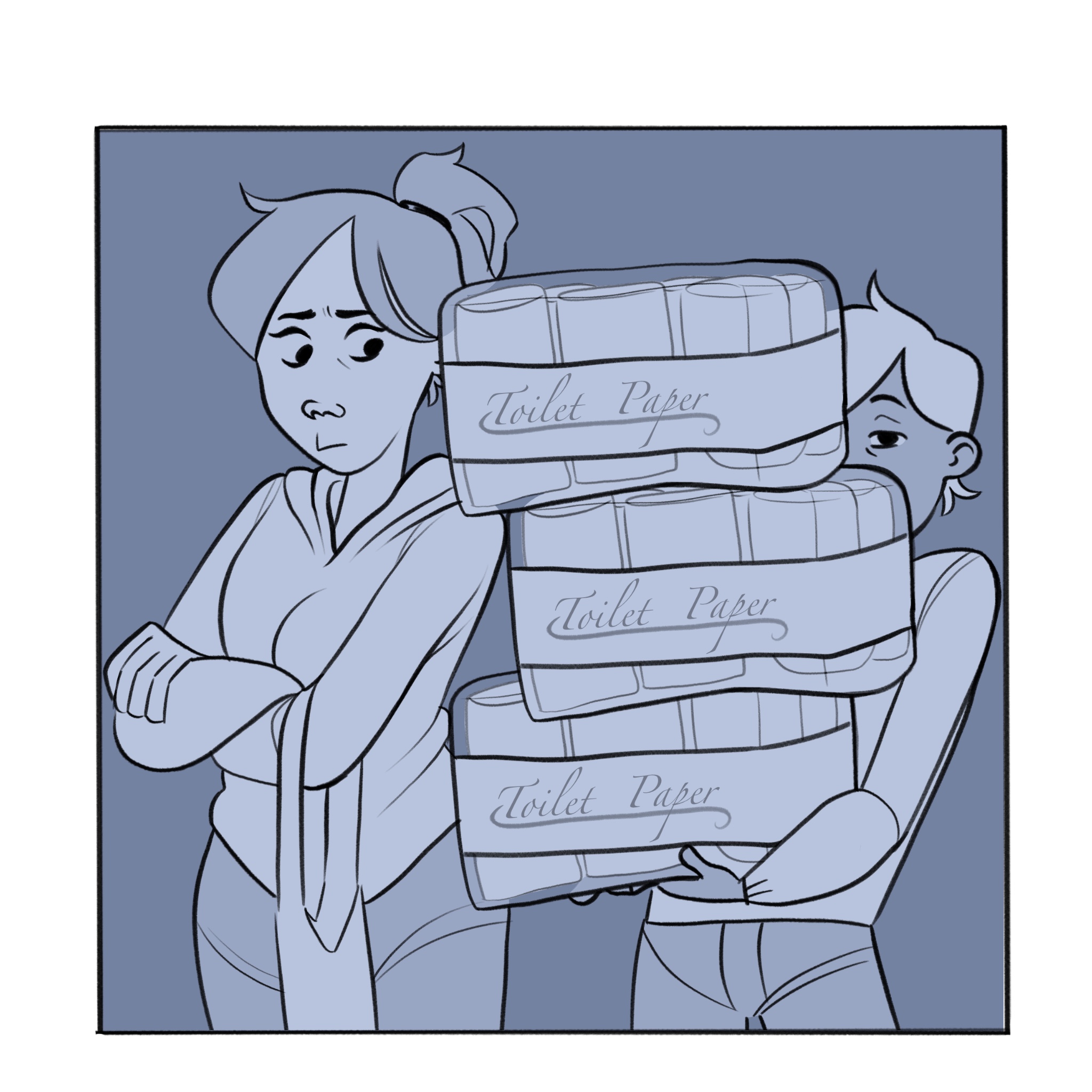

Extreme actions people are taking in times of pandemic, like bulk buying toilet paper, can put strain on the economy.

Worldwide concerns around COVID-19 have caused several countries to ban global services with citizens bunkering down in their homes. Intended as a precautionary measure for the intensifying pandemic, it has led to an economic recession.

The recession involved the worst week for Wall Street since 2008 after the Dow Jones Industrial Average, which is a stock market index that measures stock performance of large companies, declined by more than 4.4 percent in the beginning of April, with unemployment increasing 30 percent, according to BBC News. It has fallen again in the past week by 2.7%, the fall driven by the collapse of oil prices, said Market Watch. The food industry is one of the areas hit hardest by COVID-19 as it is predicted that 7 million jobs at maximum could be cut.

Andy Jenkins, executive advisor of Raymond James Financial Services, claims that decreased consumer spending is one of the problems.

“70 percent of the U.S. economy is consumer spending,” Jenkins said. “If people are staying at home and not going to bars, restaurants, movies or taking airplanes, that’s a lot of consumer spending that is no longer taking place. [Therefore,] businesses aren’t receiving [as much] money.”

President Donald Trump has been criticized for this economic crash due to ignoring the pandemic at first and claiming that the country would be fine.

“I can’t really blame him because at a certain point I was thinking the same way,” said senior Joydeep Singh. “I [thought] that this [pandemic] was going to die very soon and that we [weren’t] going to see a huge concern in the United States over this. But obviously he downplayed it at first [and it] could have been beneficial if he did some steps sooner. But another thing is that if we had done them sooner, it would’ve seemed like we were hurting the economy for no reason, because at that point there weren’t that many cases in the US to justify it.”

The emotional response has also put a strain on finances as people quickly take action to prepare for the incoming weeks of COVID-19 spreading.

“The hysteria makes people take extreme actions that businesses aren’t ready for,” Jenkins said. “[Many are] trying to pull cash out of banks, sell all of their stocks, go to grocery stores and hoard food. That type of activity puts a strain on the economy because [industries like] grocery stores weren’t expecting that much purchasing of their items and now they’ve got to restock really quickly to have food.”

The difficulty of these endeavors to make quick restocks are further exacerbated by the global trade that is declining.

“Because of shortages in supplies, people that need to produce our goods and ship to our locations are not capable of doing that either in full quantity or on time,” said Richard Groenenboom, head of Global Clinical Supply Management in Roche Pharmaceuticals. “We didn’t have to anticipate [the pandemic], so incoming goods are partially restricted and make our life a little more difficult. There’s also restrictions on outgoing goods that we produce somewhere and need to send to other countries around the world using railways, ships or planes.”

To help employees work while combatting the effects of the economic recession, human resources business partners are trying to mobilize company sites.

“Knowing that we have to follow the guidelines that the government is putting in our way, we have to make sure that we look at the impacts to people and be able to deliver our products in a different way than before,” said Nicky Rowe, principal human resources business partner of Genentech. “The impact to people would be their pay, making sure they have the transportation and support needed to get them on [campus] and that the area is clean so that they don’t pick up any infections. [Therefore,] what we’re asking our leaders is to allow more space and be kind to employees at this time as they adjust to the new ways of working.”

Despite the economic decline and unrest across the world, there is still a message of hope that all of it will be fixed as the COVID-19 crisis will end eventually.

“We’re going to come out of this more knowledgeable about viruses with better vaccines, treatment, lower interest rates and a lot of government spending,” Jenkins said. “All of that is going to make us a better country with a stronger economy. Instead of getting hysterical, buying hoards of food and taking cash out of banks, [we should] use that cash to invest in the economy that’s going to be a lot stronger in the future.”

In light of the people and businesses that have been suffering during this time, President Trump signed a relief bill in early April worth a record $2 Trillion including hundreds of billions of dollars for cheap loans to businesses, a $1200 grant to individuals earning less than $75,000 a year, and expanded unemployment benefits. Congress is now debating additional relief funding.